If you’ve experienced the burden of student debt, you’re in good company. There are more than 45 million Americans in the same boat, and student debt in the US has swelled to $1.8 trillion dollars.1

How do you help your child avoid the burden of student debt? How do you do it while you pay the bills? Save for your retirement? Pay off your own student loans?

The most important thing to recognize is that there’s no “one-size-fits-all” solution. Everyone has different expenses and priorities, and that’s okay.

Saving for College vs. Saving for Retirement

Trying to save for your child’s education at the expense of everything else may be unwise. First and foremost, work toward accumulating an emergency fund of at least a few months’ living expenses, because it’s always a good idea to be prepared for a rainy day. Then, consider your own retirement fund.

If you haven’t been contributing to a retirement plan, start today. Contributing early and often allows for compound interest to work its “magic” most effectively. And if your company offers a 401(k) match program, make sure you’re contributing at least enough to get the full company match. Otherwise you’re throwing away “free money.”

It may be tempting to put your child first and forego contributing to your retirement, but you can’t borrow for retirement, and you need to look out for yourself, too. The most prudent approach is to save for both as best you can.

Saving for College vs. Paying off Your Student Loans

If you’re still juggling your own student loans, first, take stock of what you owe. Organize your loans by lender, size, and interest rates. Can you consolidate your federal loans? Are you able to refinance your private student loans for a more favorable interest rate?

If you work in a field that may offer federal student-loan forgiveness, such as teaching or nursing, explore what you need to do to receive the benefits. Some private companies have introduced the benefit of matching whatever you contribute to your student debt per month in your 401(k), up to a certain limit. When you’re searching for your next job, this may be something to look for.

If none of these options applies to you, one of the most effective ways to pay down your own student debt is to accelerate the payments, even if it’s only a little bit. Or use a windfall, such as an annual bonus or a holiday gift, to chip away at the principal.

Once you have a handle on your own finances, however daunting that may be, you can take the first step toward saving for your child’s education.

Did You Know?

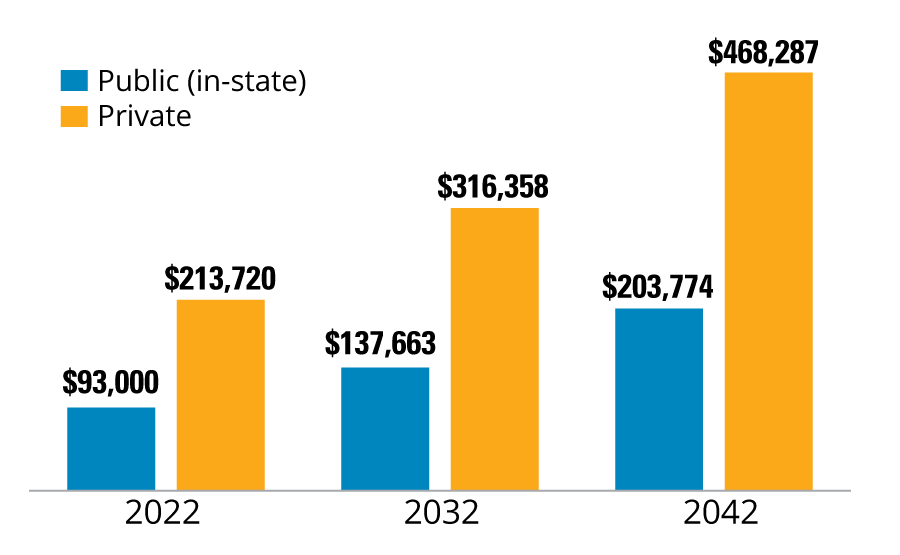

Average total costs and projected costs of 4-year college tuition, room, and board:*

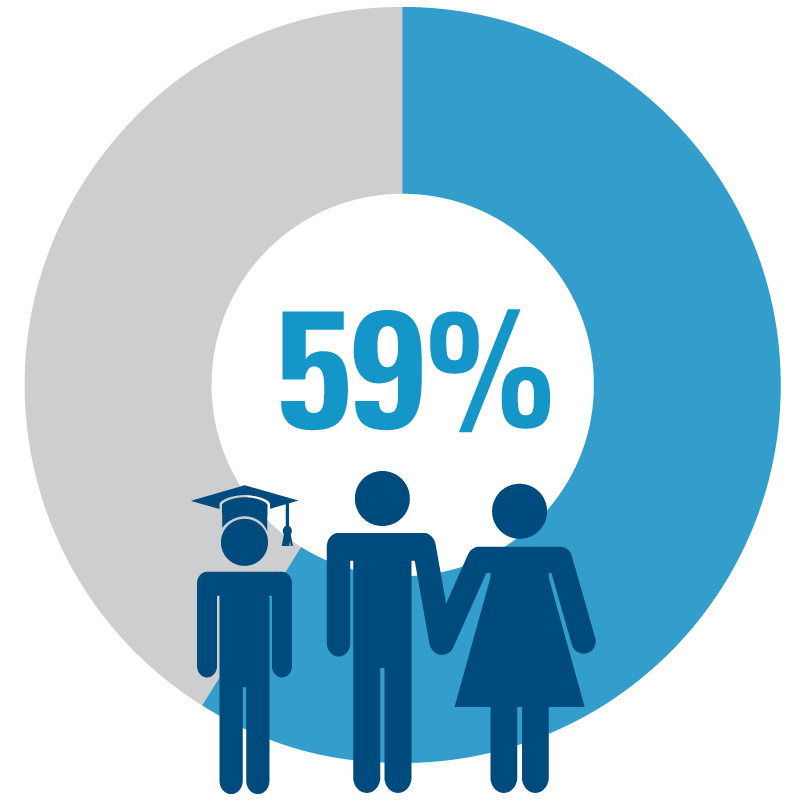

59% of families have a plan to pay for all years of college:†